CHAPTER 13

USING TITLES AS COLLATERAL TO OBTAIN DEVELOPMENT CAPITAL

13.0 Introduction

13.0.1 Context

13.0.2 The purpose of this chapter

13.1 This example; PIOs and POT graphs

13.1.1 The storyline of the example

13.1.2 The PIOs and their POT graphs for past, desired and feared future performance

13.1.3 Comments from sector groups

13.2 The system where performance is to be understood

13.2.1 The main segments of the system where performance is to be understood

13.2.2 A SCS (schematic of the core structure) of the system where performance is to be understood

13.2.3 What the SCS is indicating,qualitatively,about the dynamics

13.2.4 Scenarios to be explored in the quantitative model

13.3 The SD model and Scenario Results

13.3.1 The SD model

13.3.2 PIOs, KPIs & PIs to compare results from the Scenarios

13.3.3 Results from the model for the scenarios

13.3.4 What the Scenarios are indicating

13.3.5 Main Takeaways from the Scenarios

13.4 The Evidence that Titles as Collateral Raises Considerable Development Capital

13.4.1 Some evidence from developed countries

13.4.2 Some evidence from developing countries

13.4.3 Conclusions

13.5 Pointers for Strategy and Risk Management

13.6 Results from a briefing to PGov officials

13.7 Other Points

13.7.1 Model purpose, limitation, fitness

13.7.2 Things that could be included in further passes of the model

13.7.3 How this model could be integrated with models from previous examples

13.8 Key Points

Tables

13.1 Impact summary on the property market of the 12 land projects in ECA countries

13.2 Major risks and actions to manage

Figures

13.1 POT graphs of the PIOs

13.2a A very high level schema of the LR and Bank

13.2b A high level SCS of the LR and Bank

13.2c A high level SCS of the LR and Bank with inflows and outflows

13.3 PIOs, KPIs and PIs

13.4 POT graphs of the PIs

13.5 Results from the scenarios

Annexes

A. Major conclusions from examples in Chapters 11 & 12

B. Views of various sector groups on using titles as collateral to obtain a bank loan

C. Fig 13.2c - A SCS (schematic of the core structure) that could guide a modelling

D. Qualitative comments on the dynamics from the SCS (schematic of the core structure)

E. Fuller description of scenarios

F. Some points re evidence of titles being used as collateral

G. Abbreviations used

CHAPTER 13

USING TITLES AS COLLATERAL TO OBTAIN DEVELOPMENT CAPITAL

13.0 Introduction

13.0.1 Context

In developed countries considerable sums of development capital are raised by banks accepting property titles as collateral. This happens routinely, largely unnoticed and is taken for granted.

In developing economies banks may be largely unwilling to accept titles1 as collateral because of concerns with the Quality of titles (e.g. correctness, currency, etc). Titleholders are therefore unable to raise development capital by this means.

13.0.2 The purpose of this chapter

The purpose of this chapter is to provide a simple example: -

- Of “exploring” the quantum of development capital that might be raised if Quality of Titles2 was deemed by banks to be sufficiently high for them to routinely accept titles as collateral

- Examining the effects of-

- differrent lending policies that the banks may adopt

- the LR (land registry) being unable to sustain the very high rating of Quality of Titles required by banks for collateral lending

13.1 This example; PIOs and POT graphs

13.1.1 The storyline of this example

Setting

A large province where there are a number of LRs and a large number of properties yet to be formally registered.

Background

Senior provincial government (PGov) officials used a SD model to model to better understand the implications of treating quality as being composed of a number of subcomponents, where some are the responsibility of different agencies; the examples in Chapters 11 and 12 refer. Annex A summarises the main conclusions. The province is currently seeking aid to conduct a pilot in one LR, with a view to rolling out to all LRs.

Current situation

The senior PGov officials have now turned their attention to better understanding the raising of development capital when banks are willing to accept title documents from a LR as collateral for a mortgage.

They have again retained the service of the IC (in country) consultant with SD (strategy dynamics) skills to work with them to produce a simple SD model.

The purpose of the SD model and analysis is for senior PGov officials to better understand, at a high level: -

- The system that might have banks accept tiles as collateral, produce development capital, and have mortgages registered on the title by the LR.

- The order of magnitude of development capital that might be raised, and the % of titles that could have a mortgage

- The likely impact on a LR of having a new work stream of registering mortgages

- What might happen if the LR could not cope with the additional work, and if the rating of Quality of Titles, then dropped to a level unacceptable to the bank, for accepting titles as collateral

- The key issues involved

The above would be done with a view to the senior PGov officials then meeting with senior bank officials to explore the possibility and potential of banks being willing to accept titles as collateral for a loan.

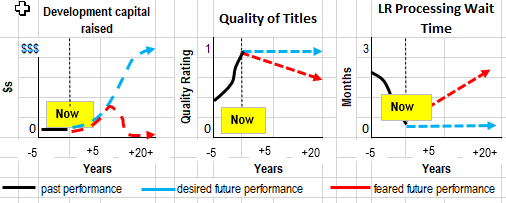

13.1.2 The PIOs and their POT graphs for past, desired and feared future performances

Following previous examples, the first step in applying the SD approach is the stating of PIOs (performance improvement objectives) and the compilation of their POT (performance over time) graphs for past, desired and feared future performances.

PIOs (performance improvement objectives)

The PIO are: –

- To raise development capital from banks accepting titles as collateral

- To maintain Quality of Titles at a very high level3 (once reached as a result of the pilot and roll out)

- LR processing wait times to remain very low4 (once reached as a result of the pilot and roll out)

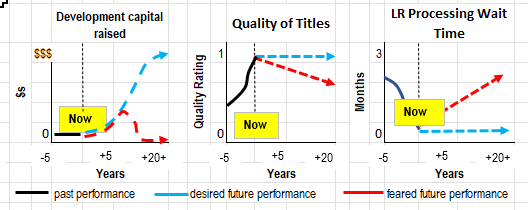

POT graphs for the PIOs showing past, desired and feared future performance

The POT graphs in Fig 13.1 for the PIOs are indicative and were compiled by the IC consultant in discussion with the LR managers and PGov officials.

Fig 13.1

Comments on Fig 13.1

- The horizontal axis is time in years and not to scale. A 20+ year time scale is taken to cover the term of a mortgage

- NOW is when the Quality of Titles has reached its target value of 0.95 and banks have agreed to commence accepting titles as collateral as normal practice, subject to their lending criteria

- The time before NOW is when the pilot to increase Quality of Titles occurs

- The desired future trajectory for development capital raised may only grow gradually. Factors affecting the speed include

titleholders becoming aware of the benefits and risks of using a title as collateral, and banks initially tending to lend cautiously.

13.1.3 Comments from sector groups

The IC consultant held discussions with: - LR managers and senior PGov officials; local banker contacts; NGOs with an interest in land; and business groups seeking their views on using titles as collateraltoobtain a bank loan. Their detailed views are shown at Annex B. A summary follows.

Summary of views

- Most groups were unaware of the potential for a title to be used as collateral for a loan, or of the amounts of development capital that are routinely raised in developed economies

- There is low trust in the LR, its operations and records. This would need to significantly change

- There were concerns that if such credit was made available, without very wide education campaigns and consumer safeguards, many titleholders, particularly small ones, could lose their property, or noting the risk, would not be willing to use a title as collateral. Banks were also concerned that, without very wide education campaigns and consumer safeguards, banks may be unable to foreclosure because of widespread community anger.

- The decision on whether or not to accept a title as collateral lies completely with the bank.

Implications for Senior PGov officials

The above reinforced to the senior PGov officials the vital necessity: -

- For success of the pilot to significantly increase Quality of Titles, by increasing the various subcomponents of quality, and to roll this improvement out to the other LRs

- To convince LR customers, business, and the community that the LRs are “trusted organisations”

- To commence engagement with the banks

13.2 The system where performance is to be understood

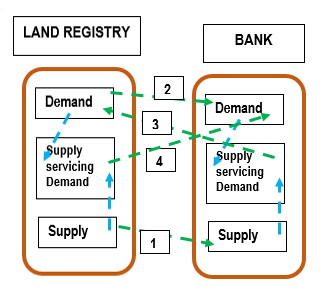

After compiling the POT graphs for the PIOs, the next step in the SD approach is to identify the system where performance is to be understood, and to compile a SCS (schematic of the core structure). In this example there are two independent organisations, the LR and the bank. They have no operational connections when banks do not accept titles as collateral. In previous examples there has only been one organisation, a LR, comprising three segments of demand, supply, and supply servicing demand, with connections between these three segments.

13.2.1 The main segments of the system where performance is to be understood

Each of these two organisations, the LR and the bank, have their own internal segments of demand, supply, and supply servicing demand. Since the aim is to better understand the system that would enable titles to be used as collateral, there will need to be “operational connections” between these, initially standalone organisations.

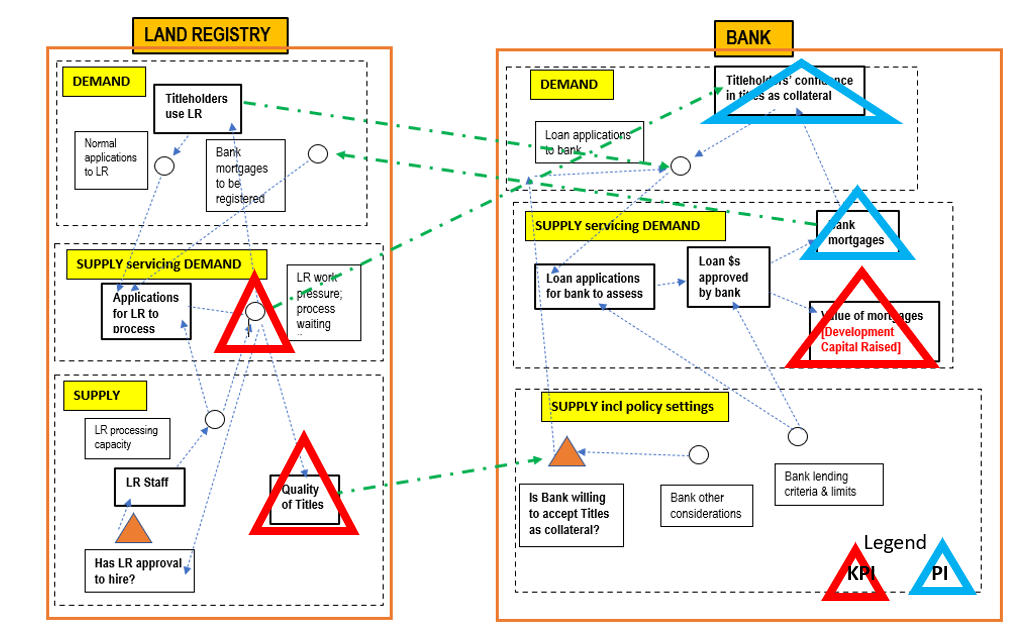

A very high level schema of the system of the two organisations

Fig 13.2a shows a very high level diagram of the system. The blue lines indicate operations internal to each organisation The green lines portray operational connections that need to be made between these two, independent organisations, if titles are to be used as collateral operationally.

Fig 13.2a

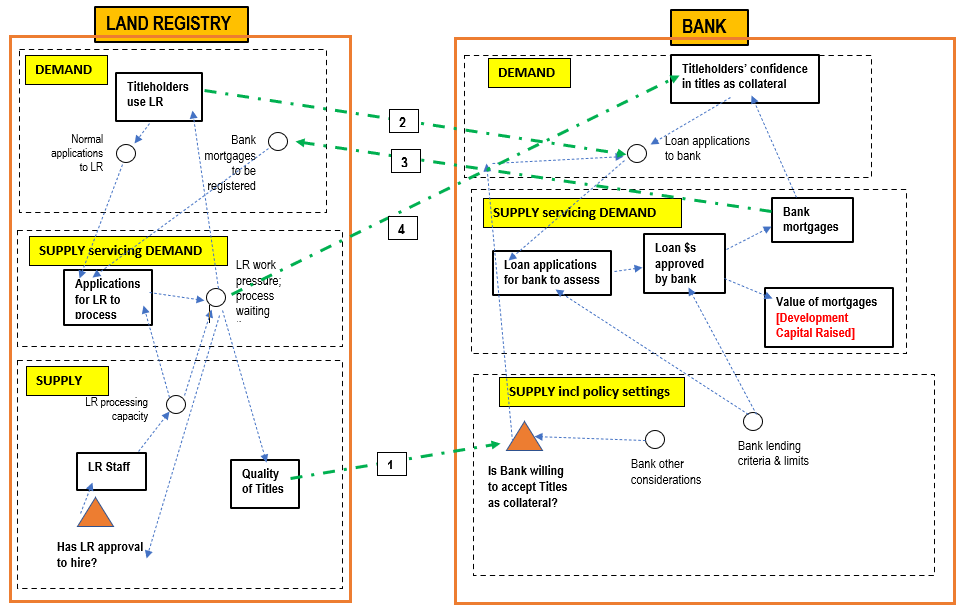

13.2.2 A SCS (schematic of the core structure) of the system where performance is to be understood

Fig 13.2b shows an expanded Fig 13.2a, still at a high level. The main stocks are shown by rectangles without their inflows and outflows. It allows the main dynamics to be seen. Qualitative observations on the main dynamics are in Sec 13.2.3.

A more detailed SCS is shown as Fig 13.2c in Annex C. Such a diagram could be used to guide modelling. The inflows and outflows of stocks are shown, as are some graphical functions.

Fig 13.b

13.2.3 What the SCS is indicating,qualitatively,about the dynamics

The following gives the major qualitative points re the dynamics that can be drawn from Fig 13.2b or c. More detail is provided in Annex D.

Major points re the dynamics

- The connections between banks and the LR (the green lines in Fig 13.2b) only become operational IF:-

- the rating for quality of titles is acceptable to the bank (green line 1)

- other conditions (e.g. titles as collateral makes business sense) are met

- The quantum of bank approvals and the amount of development capital raised, will depend upon:-

- the lending criteria of the banks

- titleholders’ confidence in titles as collateral

- the rate of loan defaults and repossessions by the bank

- the LR maintaining Quality of Titles at a very high rating, acceptable to the banks

- In the LR, maintaining a very high rating for the Quality of Titles is dependent on:-

- the LR having spare processing capacity to allocate to the maintenance of quality

- on there being approval to hire additional processing staff when demand is close to supply

- Bank approvals for loans based on titles as collateral, adds another work stream to the LR (green line 3), as mortgages need to be registered against the titles.

- If the LR is not given approval to hire additional staff to handle the new work stream of registering mortgages, and to also handle growth in normal applications, then work pressure in the LR will increase, as will processing waiting times, which will cause:-

- a decrease in Quality of Titles

- some titleholders to cease using the LR,

- a loss in titleholders’ confidence in titles as collateral, in turn causing a decrease in loan applications.

- banks to likely cease accepting titles as collateral, thus cutting off titles as collateral as a source of development capital, as the Quality of Titles has fallen below some threshold value set by the banks

Takeaways re potential strategy and risk management

Some points re potential strategy and risk management can be drawn from the qualitative major points above:-

- The imperative for Quality of Titles to be maintainedby the LR (and associated agencies) at the very high level required by the banks

- The decision on whether or not to accept titles as collateral, lies solely with the bank

The above also follows on from the implications for senior PGov officials drawn in Sec 13.1.3. [Quantitative results from the model are shown in Sec 13.4.3 and observation and takeaways discussed in Sec 13.4.4].

13.2.4 Scenarios to be explored in the quantitative model

At this stage in previous examples, PIPs (proposals to improve) were brainstormed and listed with values for the main variables. In this example the scenario feature of Silico, the simulation software, will be used. This allows the establishment of a base case, and the setting of different value for the main variables for the different scenarios. In this case the main variables are mostly the bank’s lending criteria.

The IC consult ant identified the following scenarios to be “explored” when a model was built.

- Base Case -Banks do not accept titles as collateral

- S1-Banks lend very conservatively; LR maintains a very high Quality of Titles

- S2-Banks lend less stringently; LR maintains a very high Quality of Titles

- S3-S2 + an increase in titleholders; LR maintains a very high Quality of Titles

- S4-S3 BUT LR unable to maintain a high Quality of Titles

Annex E contains a fuller description of each scenario, together with values used for the main variables

The aim is to provide the senior PGov official with a better understanding of the system which could provide development capital, if banks were willing to accept titles as collateral.

13.3 The SD model and Scenario Results

13.3.1 The SD model

The IC consultant built a SD model based on the SCS of Fig 13.2c and the scenarios listed in section 13.2.4 and Annex E. As noted in previous chapters, it is not the purpose of this book to go into the mechanics of building an SD model, but rather to show how operational insights can be drawn from using a model. Those interested in the model itself should contact the author at [email protected].

13.3.2 PIOs , KPIs & PIs to compare results from the Scenarios

The three PIOs are by definition KPIs (key performance indicators) of the system. They are:- development capital raised; Quality of Titles; LR processing wait time. These KPIs/PIOs are annotated on Fig 13.3, which is the SCS of Fig 13.2b.

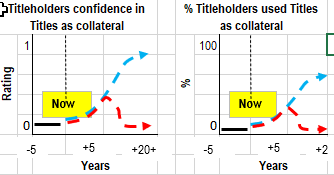

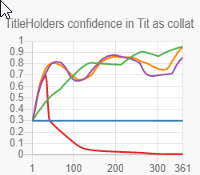

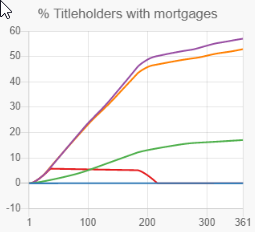

An examination of the SCS allows the identification of an additional two PIs (performance indicators). They are:- Titleholders confidence in Titles as collateral; % Titleholders used. These PIs are also annotated on Fig 13.3. POT graphs for these PIs are shown as Fig 13.4.

Fig 13.4

NB- Where KPI/PIs are stocks (as most are in this example) it is worth remembering that the value of a stock at any time is dependent on the rate of their in and outflows, and what in turn affects them. Thus flow rates are very important.

Fig 13.3 KPIs and PIs

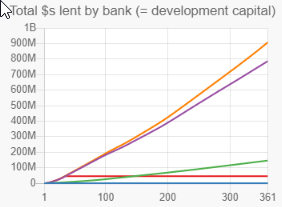

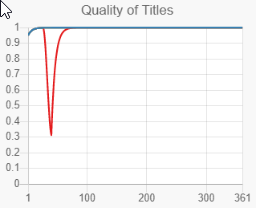

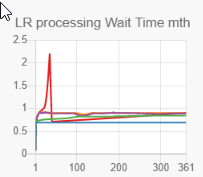

13.3.3 Results from the model for the scenarios

Row 1 in Fig 13.5 shows the POT graphs (of past, future desired and feared trajectories) for each of the PIOs/KPIs (from Fig 13.1) and PIs (from Fig 13.4). The part of these graphs that are of interest is from NOW (thick black line refers) forward, showing the desired and feared futures. NOW is the time when the Quality of Titles reaches a very high rating that is likely to be necessary for banks to accept titles as collateral. The high rating for Quality of Titles and the decrease in waiting time is achieved via the pilot and roll out to significantly increase quality, where quality is treated as having subcomponents.

Row 2 shows the results from the model for the base case and the four scenarios, for each of the PIOs/KPIs and PIs. The time axis is in months, and the simulation runs for 360 months (30 years), which should cover the loan term where a tile is used as collateral, and to examine sustainability. NOW is month 1(thick black line refers).

Fig 13.5

Row 1 PIO/KPI PIO/KPI PIO/KPI PI PI

Row 2

Base Case: Banks do not accept titles as collateral Scenario 1 (S1): Bank lends cautiously; LR maintains high quality

S2: Bank lends more; LR maintains high quality S3 is S2 + Titleholders increase due to subdivision

S4 is S3 + LR does NOT maintain high quality

13.3.4 What the Scenarios are indicating

Examining the graphs in Fig 13.4, allows observations to be made on the likely efficacy of each scenario.

Base Case, Banks do not accept titles as collateral. As expected, this scenario does not result in any development capital being raised, or any titleholders having mortgages. LR processing wait times remain very low as the LR has sufficient processing capacity to deal with normal demand. The Quality of Titles is high, due to the prior aid project which raised quality, and the LR being able to keep the quality high due to having sufficient capacity for maintenance.

Scenarios S1,S2,S35.All scenarios largely produce similar results, differing only in quantum for the PIO/KPI, development capital raised, and the PI, % titleholders used titles as collateral. The differences are due to the bank’s lending policies. S1 has very conservative lending, while S2 has less stringent lending, and S3 is S2 with an increase in titleholders. The PIOs/KPIs, Quality of Titles, and LR processing wait time, remain respectively very high and very low, in line with their desired future trajectories shown in Row 1. For the PI, titleholders confidence in titles as collateral, the trajectories are in line with the desired future depicted in Row 1. The small oscillations are due to short term losses in titleholders confidence when loan defaults and repossessions occur.

ScenarioS4,S3 BUT LR unable to maintain quality. This scenarioproduces quite different results from S1,2,3. It essentially produces the feared future trajectories depicted in Row 1. The PIO/KPI, Quality of Titles, after a relatively short time, suffers a very large drop in quality rating due to the Finance Department not approving the use of a small % of LR revenue to fund extra LR staff to handle the extra processing of registering mortgages on titles, and to maintain quality.

LR supply capacity thus cannot service LR demand, work pressure increases, LR processing waiting time (a PIO/KPI), quickly increases, and Quality of Titles (a PIO/KPI) significantly decreases. When the Quality of Titles drops lower than 0.8 for 3 consecutive months (from the target value of 0.95), the bank loses confidence in the PGov/LR ability to maintain quality over long periods and hence decides to cease lending using titles as collateral.

This leads to titleholders confidence in titles as collateral (a PI), quickly dropping to zero. As the banks stopped lending early in the simulation period, only a very small amount of development capital (a PIO/KPI), was raised and only a very small % of titleholders have mortgages (a PI).

Once the work stream of registering mortgages ceases, then after some time LR capacity becomes greater than demand, and LR processing waiting time decreases, the Quality of Titles increases back to target level. However the banks are now not willing to recommence accepting titles as collateral, so titles as collateral as source of development capital has ceased.

13.3.5 Main Takeaways from the Scenario Results

The main takeaways from the scenario results are:-

- Significant amounts of development capital can be raised using titles as collateral IF banks are:-

- willing to accept titles as collateral; (having been convinced that the Quality of Titles has reached a very high level and can be maintained at that high level for the indefinite future by the PGov/LR)

- convinced that accepting titles as collateral for a loan makes commercial sense

- The quantum of development capital raised will very much depend on:-

- the lending policies of the bank

- the rate of loan defaults and repossessions

- the confidence that titleholders have in using their property as collateral for a loan

- The paramount importance for the PGov to ensure that the LR and other government agencies, which are responsible for particular subcomponents of quality, to maintain these subcomponents at their required quality rating over very long periods of decades. This will greatly depend on the Finance Department allowing the LR to maintain a small % of revenue to ensure adequate budgets and to maintain quality. (Examples of Chapter 9, 11, 12 refer).

- If Quality of Titles falls below a threshold level (say for 3 consecutive months), then banks are likely to cease accepting titles as collateral and be unwilling to restart such lending, due to a lack of confidence in the PGov and its agencies, to continuously maintain high standards of quality over very long periods of time.

- The development capital raised in this example was from one LR. The potential is much greater province wide, as there are several LRs in the province and a considerable number of properties have yet to have their property rights registered.

These takeaways are in line with the qualitative dynamics drawn from the SCS, Sec 13.2.3 refers. However these takeaways are based on the quantitative results from the SD model, Secs 13.3.3 and 4 refer. The SD model also provides the ability to change the values of variables, add additional scenarios and, if necessary, change the structure (development logic) of the model.

Other important points are:-

Consumer education and safeguards. Using titles as collateral will be a new form of lending it, hence it would be prudent for there to be a wide consumer education program, backed up by best practise responsible lending guidelines and perhaps legislated consumer safeguards. It would be in no one’s interest to have high loan defaults and repossessions, and for titleholders to lose confidence in titles as collateral and avoid this avenue of development capital.

The need for clarity in the selection of the aim when seeking to increase “quality”. In points #3 and #4 above the paramount importance of maintaining Quality of Titles at its very high target level over decades was noted. As Quality of Titles is comprised of a number of subcomponents under the control of a number of agencies, then ALL of these subcomponents must also maintain their target quality over decades. Annex A shows the subcomponents diagrammatically.

In Chapter 11, which dealt with Increasing Quality, where Quality has subcomponents which are the responsibility of different agencies, Sec 11.6.2 discussed the need for clarity in the selection of the aim when seeking to increase “quality”. As there are a number of quality subcomponents, it need to be quite clear if the aim is to increase the quality of one subcomponent, or several, or all, and what is sought to be achieved, as each subcomponent will have its own quality gap to close, with associated costs and timeframes. Also there is interdependency between some subcomponents.

13.4 The Evidence that Titles as Collateral Raises Considerable Development Capital

The IC consultant, while developing the model, did a quick online search for evidence of titles being used as collateral and also spoke to some conveyancer contacts in Australia, a developed country. The aim was only to get some indication, as more in depth research would be required if initial talks with the banks proved promising. Some points follow and other information is in Annex F.

13.4.1 Some evidence from developed countries

In developed countries, such as Australia, Canada, USA, UK it is taken for granted that if one has title to an unincumbered property, then one can approach a bank about a loan, using the property as collateral. It is also taken for granted that the information recorded on the title issued by the LR is correct and accepted by all parties. As a result, large quantities of capital are routinely raised.

The state of Queensland in Australia – April 2021

- Population ~5.2m; households ~2.0m

- 60-80% of properties have a mortgage (informed opinion)

- Monthly new loan commencements worth ~$4.1b

- Monthly mortgages documents lodged ~18,800

- Monthly title searches ~181,000

(various online sources incl ABS (Australian Bureau of Statistics) and Queensland Titles Office)

UK

Recent years

- there is approximately US$5 trillion in the value of housing and US$2 trillion in the value of commercial properties.

- the contribution from housing is 15–18% of GDP considering professionals working in the real estate sector and various rents, etc. This probably rises to over 20% when commercial property is included (The National Association of Home Builders)

- Mortgages registered at the Land Registry in England and Wales amount to over US$1.2 trillion (Land Registry Business Strategy for 2017 to 2022). [This is a huge amount of investment that has an enormous impact on the economy as a whole. Adlington et al 2021]

Adlington G, T Lamb, R McLaren, R Tonchovska (2021

1991

- ~42% of UK’s 24m residential properties have a mortgage.

- ~ 67% of UK’s credit secured with residential property

- ~57% of national wealth comprised by land & buildings

(Byamugisha (1999) referencing Munroe-Faure (1997), and Callander and Key (1997)

13.4.2 Some evidence from developing countries

Few reports were found that give information on the number and value of mortgages raised as a result of LA projects.

ECA (Europe and Central Asia) land projects

Two reports provide some numbers reported on the economic impact and lessons learnt from 20 years and 12 completed projects in ECA (Europe and Central Asia) land projects.

- The aim of the ECA land projects was, Satana et al (2014), to promote private sector development by establishing reliable and transparent registers, reduce transaction costs and make property available as collateral for loans. The aims, scope and achievements of the individual projects had some variation and summaries of each are provided in the paper. Some impact numbers on the land and property market were provided by Satana et al (2014), and also by Torhonen, M (2016). These numbers are summarised in Table 13.1. The average project length was ~ 8 years.

Table 13.1 Impact summary on the property market of the 12 land projects in ECA countries

| Indicator | Reported Values |

|---|---|

| Land Registration | |

| Number of parcels registered | 2.5m; 1.1m; 17m; 2.5m |

| Increase in urban parcels registered | 5%; 33%; 35%; 60%; 80% |

| Increase in rural parcels registered | 0%; 60%; 70%; 90% |

| Mortgages | |

| Increase in volume of mortgages | 44%; 137%; 4 times; 0 to 45k |

| Increase in value of mortgages | 3 times; 4 times; 10 times |

| Land and Property Market | |

| Increase in volume of land and property market | 4 times; 5 times; 30%; 70% |

| Increase in land and property sales | 60%; 80%; 2.5 times; 5 times |

| Investment and Tax Collection | |

| Increase in foreign investment in construction | 0.5 to 8%; €4.8m |

| Increase in tax collection | 8%; US$12.5m |

Comments on Table 13.1

- There were wide variations in impacts due to differences between countries due to size, specific aims, commencing status, specific IC situations, etc.

- Even allowing for the above, there was a very positive impact on the property market for these ECA countries over a relatively short time.

- It is possible for land projects to result in titles being used as collateral.

Torhonen, M (2016) discussed lessons learnt from these ECA land projects, and ones that are relevant to titles as collateral, are summarised in Annex F.

Nepal and Bangladesh

Subedi (2016) reported on the economic impact of land titling and land administration in a rural area of Nepal and Bangladesh and drew comparisons with an area in Thailand. For access to credit, it was reported that prior to land registration private lenders charged 40% interest in Nepal and 30% in Bangladesh, and that post registration, banks accepted titles as collateral at an interest rate of ~15%. Subedi (2016) also reported on other types of economic benefits achieved such as:- increases in the value of land; changes in land use/land zoning; increases in official land valuations; increases in owner investment in land.

However Subedi (2016) reports that malpractice in land administration can threaten tenure security and resultant benefits. It was noted that up to 80% of court cases in rural Bangladesh are related to land. Thailand was identified as having high quality land administration.

13.4.3 Conclusions

Considerable sums of development capital are routinely raised in developed countries using titles as collateral. Similar can be achieved in developing countries, but the lessons learnt from the ECA land projects, Torhonen (2016), need to be borne in mind. (Some lessons learnt are listed in Annex F).

As noted by Torhonen (2016), it is not axiomatic that economic benefits will result from LA projects. Complementary measures are likely needed (such as engagement with banks re their accepting titles as collateral).

13.5 Pointers for Strategy and Risk Management

The story line of this example (Sec 13.1.1) was that the senior PGov officials wanted to better understand the system that provided development capital using titles as collateral, with a view to the senior PGov officials then meeting with senior bank officials to explore the possibility and potential of banks being willing to accept titles as collateral.

The ultimate aim of the PGov is to have development capital raised by banks accepting titles as collateral. A strategy will be required to achieve this. This example providers pointers to that strategy. A firmer strategy would be determined sometime after engagement with the banks.

Pointers for strategy

The following are pointers: -

- PGov to ensure that all its involved agencies achieve and sustain the target ratings for the Quality of Title subcomponents for which they are responsible

- PGov to engage with the banking sector to:-

- convince the banks that the very high ratings for Quality of Title can be achieved and sustained over decades

- achieve the banks accepting titles as collateral

- provide consumer education and safeguards for all involved parties, together with mechanisms for dispute resolution

Pointer for major risks and their management

The pointers for major risks and actions to manage are shown in Table 13.2.

Table 13.2

| No. | Major Risk | Risk Management |

|---|---|---|

| 1 | The very high rating for Quality of Titles cannot be sustained, and banks cease accepting titles as collateral. | The PGov should set up mechanisms to regularly assess the quality standards being achieved and, if necessary, take quick corrective action. |

| 2 | Consumer education and safeguards are not effective, and loan defaults and repossessions occur at such a level that most titleholders are unwilling to use titles as collateral as a source of finance. | The PGov, banks and community groups should regularly monitor the rates of loan defaults and repossessions, ascertain the reasons, and take quick corrective action. |

13.6 Results from a briefing to PGov officials

The IC consultant briefed the senior PGov officials on the SD approach used, results from the model and scenarios, and the key takeaways. The senior officials considered that they now better understood and resolved to:-

- Ensure that the second pilot to increase Quality of Titles (where the many subcomponents of quality were to be increased), was a success; that success included ensuring long term sustainability, including adequate O&M (operations and maintenance) budgets; that the results of the second pilot provided a sound base for scaling up and rolling out to other LRs

- Commence exploratory discussions with the banks, re their accepting titles as collateral to generate development capital

13.7 Other Points

13.7.1 Model purpose, limitation, fitness

Model purpose

The purpose of the model (Sec 13.1.1) in summary was for senior PGov officials to better understand :-

- The system and development capital might be raised if banks were willing to accept titles as collateral

- How the rating for Quality of Title effects a bank’s decision to provide a loan to a titleholder using the title as collateral

- What might be the effect if the PGov, the LR and associated agencies could not maintain the quality rating for Quality of Title that the banks require

- The impact of an additional processing work stream, that of registering mortgages on titles, would have on the LR

Model limitations

The model has quite a number of limitations; viz: -

- It is largely based on an initial high level hypothesis of how banks will interact with the LR (PGov). While the PGov officials have built up a good understanding of the system for LR processing via previous examples, the understanding of the bank side is not so clear

- The model could not be validated as there is no past actual data as banks have yet to accept titles as collateral for loans

Model fitness for purpose

In spite of the above limitations, the model is considered fit for purpose as: -

- The senior PGov officials consider they now have a better understanding (Sec 13.7) and feel in a position to start exploratory discussions with the banks.

- It was recognized that this initial model would only be a simple first pass and further models would be necessary

- The adage all models are wrong, but some are useful applies here. The model is considered useful as it meets its purpose, to provide better understanding.

13.7.2 Things that could be included in further passes of the model

More development of the model will be necessary as discussion with the banks evolve, detail is added, real data becomes available, and market research is undertaken to determine possible titleholder uptake. The following could be included:-

- A much better representation of the bank’s system, and the development of a model that could be used jointly by the banks and the PGov /LR to further explore the potential for titles to be used as collateral

- A much better understanding, and associated data, of “success” in the AEC projects

- Some market survey to identify possible take up rates, and loan amounts sought, if titles were available as collateral

- The inclusion of increased buying and selling in the property market

- One scenario, where bank lending is quite cautious for some time and then expands responsibly

- Segmentation of loan applicants into categories such as:- major commercial; SMEs (small medium enterprises); rural property owners; urban property owners

- The inclusion of government land, held on a long term (say 99 year) lease

13.7.3 How this model could be integrated with models from previous examples

Future pass of the model could be integrated with:-

- The revised model for increasing the various subcomponents of quality (the second pilot for which the PGov is currently seeking aid to design and implement (Sec 13.1.1 and Chapter 11 refer)

- The model of Chap 9 could also be incorporated as this would allow inclusion of the LR financials [revenue to government, the % of revenue necessary to be allocated to the LR to achieve sustainability and to maintain a very high rating for Quality of Titles], as well as once off improvement costs to enable CBA (cost benefit analysis)

13.8 Key Points

- Titles are routinely used as collateral to raise significant amount of development capital in developed countries.

- There is evidence, particularly from the ECA land projects, that titles can also be used to raise development capital in developing countries. However this is not axiomatic, and the lessons learnt from the ECA projects are very important.

- The hypothetical example in this chapter showed how the SD approach was used to enable senior PGov officials to better understand the system where titles might be able to be used as collateral, and the key issues, before approaching banks for discussion.

- One very important that point came out to the PGov officials was the vital necessity to maintain over decades, the very high rating for Quality of Title that the banks require as a condition of accepting titles as collateral. This in turn meant that the LR and associated agencies which have responsibility for specific subcomponents of Quality of Title, need to maintain their quality targets over decades.

- As in previous examples, this example and the results shown, are not the most important part. The important aspect is how the SD approach can be used. If the logic and structure of the SCS or the structure of the SD model is not appropriate for a particular situation, then it is relatively simple to develop an alternative SCS and SD model and use them. The most important point is that the SD approach is logical, quantitative and transparent, with no implicit assumptions or hidden hard wiring.

References

Adlington G, T Lamb, R McLaren, R Tonchovska (2021), Real Estate Registration and Cadastre. An RICS insight paper, global.

Byamugisha, F, (1999). The Effects of land Registration on Financial Development and Economic Growth, World Bank Policy research Paper 2240

Callander, M, and Key, T, (1997). What is the value of UK property. Charted Surveyor Monthly April 1997

De Soto H, (2000), The Mystery of Capital- Why Capitalism Triumphs In The West and Fails Everywhere else. Bantam Press

Jaffee, D, and Renaud, B, (1996). Strategies to develop mortgage markets in transition economies. World Bank Policy Research Working Paper No. 1697

Jefferies, G, (1996). Value of the legal cadastre in a free market economy. Paper presented at the International Conference on Land Tenure and Administration, 12-14 November, Orlando, Florida, USA

Munroe-Faure, P, (1997). Land market, mortgage and tax experience in Central and Eastern Europe. A Paper for a Conference on Land Management in Russia entitled, Present Achievements and Future Aspects, Leningradskaya Hotel, Moscow, December 16-17, 1997

Satana S, Torhonen M, Anand A, Adlington G, (2014), Economic Impact of 20 Years of ECA Land Registration Projects, Annual World Bank Conference on Land and Poverty. Washington DC, USA. March 24-27, 2014.

Subedi G (2016), Land Administration and Its Impact on Economic Development, PhD thesis University of Reading

Torhonen, M (2016). Keys to Successful Land Administration, Lessons Learnt in 20 Years of ECA Land Projects. World Bank

ANNEX A

Major conclusions from examples in Chapters 11 and 12

Major conclusions from example in Chapters 11 - Treating quality as having subcomponents

There are various views of overall quality; viz

- Overall quality (under control of LR)

- Overall quality (of LR); Overall quality (tenure security)

- Overall quality (assist economic development).

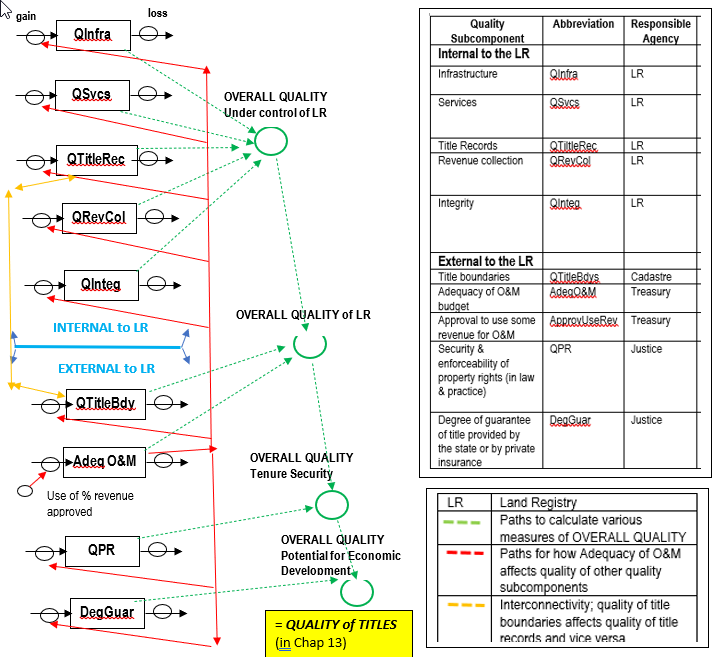

These overall measures are derived from a number of quality subcomponents, some being under the control of the LR and others under the control of a number of other government agencies. [Sec 11.2, Table 11.1, Figs 11.2, 11.5 refer.] Fig 11.5 below shows the subcomponents of Quality and how they were combined to provide the various views of Overall quality. NB- there is interdependency between some of the subcomponents.

Fig 11.5

If the improvement aim is increase Overall quality (tenure security) and/or Overall quality (assist economic development) then it is vital to have the other agencies involved that are responsible for particular subcomponents of quality; without their involvement, target values and resultant benefits will not be achieved.

Increasing the quality of subcomponents to target values with aid assistance, whilst having challenges, will probably be relatively straightforward. Maintaining the increased quality post aid will largely depend upon the necessary IC funding to maintain that quality at target values, being made available consistently over long periods of time. If the necessary maintenance funding is not provided, then quality will decrease, and the value of the improvement investment will also decay over time6.

Close attention needs to be given to the effects of long delays before quality targets are achieved. A common reason for long delays is the wait for legislation to be enacted and operationalised.

Major conclusions from example in Chapters 12 - Addressing Informal fees

When customers are asked by staff to pay informal fees, such as go fast fees, in addition to the normal legal fees, this has an adverse impact on the LR quality subcomponent, integrity of operations. This in turn effects Overall quality (of LR), Overall quality (tenure security) and Overall quality (assist economic development).

Improvement endeavours to negate informal fees have risks as informal fees may be a wide spread and of long standing practice. The risks need to be closely managed. Success may take some considerable time, and some scenarios indicate that success may not be achieved.

Addressing informal fees can be considered as integral to LR quality subcomponent, integrity of operations.

Recap – Importance of the LR/ RGL

When discussing what land administration (LA) is, (Sec 2.1.1 refers), it was stated that three of the goals of LA were to:- provide secure and enforceable property rights; contribute to social well-being and stability; contribute to economic development.

A Land Registry (LR) (Fig 2.2 refers) is a key organisation underpinning these three goals as they hold the titles that document the property rights and interests held by various parties. Commonly the parties are the property owner, and the holder of a mortgage on the property, but it can get complex.

The purpose of the LR is to hold correct and current records of private property rights, and for all property dealings to be conducted via the LR so ensuring that tenure is secure, and formal lending institutions can rely on the veracity of LR records when considering whether or not to accept a property as collateral for a loan.

A RGL (register of government land) (Fig 2.2 refers) has a similar purpose to a LR, but for government land. It is common for government land to be leased and for lease holders to pay a once off fee as well as an annual fee.

A LR and RGL will only deliver significant benefits if their overall quality is very high and titleholders, the community and business also have high confidence in the correctness of LR/RGL titles and the integrity of their operations. Sec 11.2.1 refers.

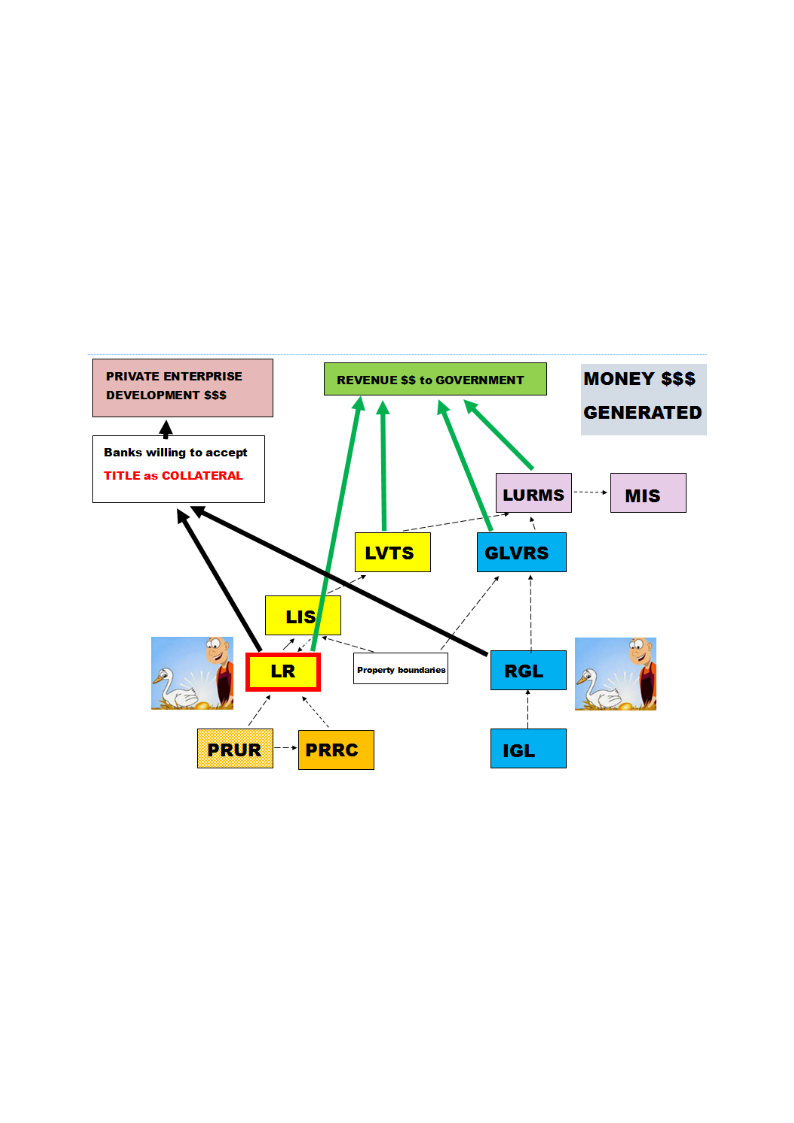

Fig 2.5, shown below, shows the Revenue to Government, and Development Capital made available by using property title as collateral. It also shows the downstream LA operational entities that can be based on data from the LR and RGL.

Fig 2.5

ANNEX B

Views of various sector groups on using titles as collateral to obtain a bank loan

From the perspective of LR/LO

- Banks, titleholders and business have never raised as an issue, any desire to use titles as collateral.

- Our job is to process applications that are submitted

From the perspective of banks

- Titles and recorded property right are not considered as sufficiently reliable, secure and enforceable to be acceptable as collateral. The reputation of the LO/LR for the integrity of its operations is not that high.

- The decision on whether or not to accept a title as collateral lies completely with the bank.

- A bank’s lending criteria may well follow the four Cs:- Collateral (has sufficient value); Character (will person do their best to repay); Capacity (person has the ability to meet repayments); Conditions (special conditions that bank may impose).

- Bankers have concerns that many titleholders would not fully understand their loan obligations, and the banks right to repossess if default occurred. If default occurred and banks tried to repossess, there could be widespread local community anger, making repossession not feasible.

- There would have to be considerable improvements in the Quality of Titles and the integrity of LO/LR operations, before the banks would consider regularly accepting a title as collateral as a worthwhile business opportunity, in any but special cases.

From the perspective of land NGOs

- There is low community trust in the LO/LR, its operations and records.

- Many land/ property owners fear that if they used their title as collateral for a loan, there would be a real danger that they could lose their main asset in life, their land/ property.

From the perspective of a Business Group

- Don’t understand enough about this source of development capital, but it sounds as if there is a lot of potential and they would like to understand more.

- The reputation of the LO/LR, its integrity, operations and records is not that high and that would need to change.

- There would need to be education of and safeguards for consumers.

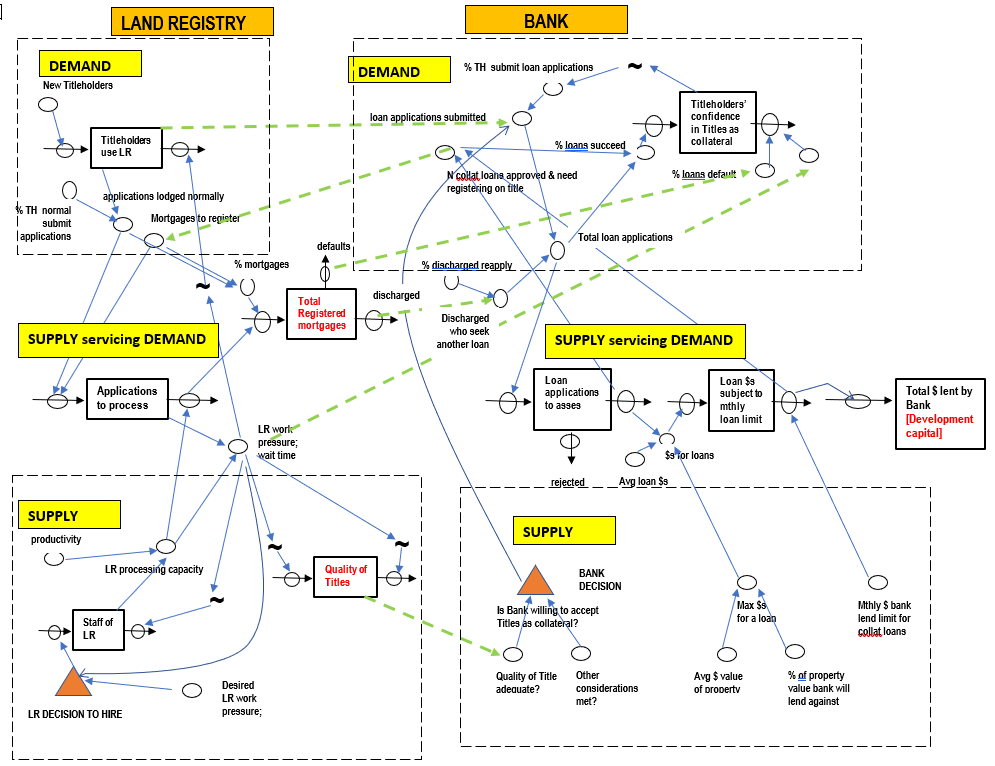

ANNEX C

Fig 13.2c - A SCS (schematic of the core structure) that could guide modelling

ANNEX D

Qualitative comments on the dynamics from the SCS (schematic of the core structure)

[The following refers specifically to Fig 13.2c in Annex C. However it also generally applies to Fig 13.2b.]

Initially, where the banks do not accept titles as collateral, then the LR and banks operate as completely separate organisations. There are no operational linkages between them as depicted by the green lines.

If the banks accept titles as collateral, then there is a linkage as shown by the green dashed line A linking Quality of Title (a stock in the LR) to the bank’s decision to accept titles as collateral, subject to the rating of Quality of Title being at some very high level acceptable to the bank, and also any other bank conditions being met, such as title collateral lending making commercial sense

Once banks decide to accept titles as collateral, the blue solid line B shows that this triggers the acceptance of loan applications from titleholders. The green dashed line C shows the linkage from the stock of Titleholders using the LR to the loan applications submitted to the bank.

The % of titleholders who submit applications will be influenced by the stock, Titleholders confidence in Titles as collateral. As titleholders confidence increases so will the % of titleholders who submit applications for loans. Titleholders confidence will increase as they see loan applications from other titleholders being successful. Titleholders confidence will decrease as loan defaults occur or increase to a significant level, and also if there are delays in the LR to register mortgages on titles, and work pressure in the LR increases.

Loan application submitted to the bank then have to be assessed according to the bank’s lending criteria and policy settings. This process is depicted in the bank’s segment of Supply servicing Demand.

The lending criteria and policy settings of the bank are shown in the bank’s segment of Supply (including policy settings). The following are included in this section. The bank’s decision on whether or not to accept titles as collateral, as discussed above. A number of other policy settings which together set the bank’s lending criteria. The % of loan applications that pass assessment. The maximum amount of an individual loan that the bank will consider, being determined by the average value of the property, and the percent of property value that the bank is willing to lend against. The maximum $ amount per month that the bank is willing to lend where titles are used as collateral. Lines connect these policies settings to relevant parts depicted in the bank’s segment of Supply servicing Demand. The staffing of the bank for processing the loan applications for titles as collateral is not shown as insufficient is known at this stage, and it is not required for the purpose of the model in this first pass.

In the bank’s segment of Supply servicing Demand, loan applications are first assessed by the stock and flow structure of loan applications to assess, and successful loan applications are then subject to the stock and flow structure of $ of loans subject to monthly $ loan limit. Those loans that are approved then determine the development capital that has been raised (one of the PIOs) via the accumulating stock, Total $s lent by bank [= development capital].

Once the loan and the loan amount has been approved by the bank the mortgage has to be registered by the LR and this connection where it enters the LR processing system is shown by the green dashed line D. When the mortgage has been registered it enters a stock labelled Total registered mortgages. This is where the number of mortgages is tracked. Mortgages cease due to being discharged based on the average mortgage duration. A certain percentage of discharge mortgages may reapply for a new mortgage and this is shown by the green dashed line E. Mortgages also cease where loan defaults occur. A high loan default rate can cause titleholders to have a loss of confidence in titles as collateral (a stock). This connection is shown by the green dashed line F.

The loans, using titles as collateral, that have been approved by the bank, have to be registered as a mortgage on the titles, and this adds another work stream to the LR. This adds to the total number of applications that need to be processed. If LR/PGov management approved the hiring of additional staff when required then work pressure is acceptable, waiting times for processing remain low and there is sufficient capacity to ensure that Quality of Titles remains at a very high level. If LR processing capacity is insufficient, then the work pressure will increase, and the backlog and waiting time will increase. Long waiting times can cause some titleholders to cease using the LR. High work pressure can affect LR productivity, and also cause a decrease in Quality of Titles. A decrease in Quality of Titles to the lower limit acceptable to the bank, could lead to the bank deciding to no longer accept titles as collateral, and hence development capital from that source would cease.

ANNEX E

| Scenario | Scenario Name | Outline |

|---|---|---|

| — | Base Case — Banks do not accept titles as collateral |

|

| S1 | Banks lend very conservatively and LR maintains a very high Quality of Titles. |

|

| S2 | Banks lend less stringently; growth in titleholders occurs and LR maintains a very high Quality of Titles. |

|

| S3 | S2 plus an increase in titleholders; LR maintains a very high Quality of Titles. |

|

| S4 | S3, but LR is unable to maintain a high Quality of Titles. |

|

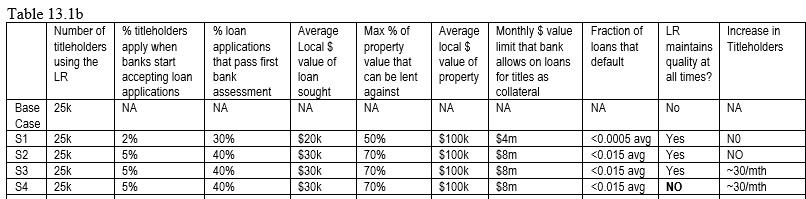

The table below indicates some values for key variables in the SCS of Fig 13.2d that the IC used in a first pass of the model.

ANNEX F

Some points re evidence of titles being used as collateral

Developed Countries

- The link between real estate registration and economic growth has been made for many years, with The Economist on 29 May 2003 stating that ‘land and property markets, including construction, may contribute as much as 15 per cent to GDP in a developed economy’.

Adlington G, T Lamb, R McLaren, R Tonchovska (2021), Real Estate Registration and Cadastre. An RICS insight paper, global.

USA – early/mid 1990

- the mortgage market is amongst the largest components of the financial markets with mortgage debt estimated at US$4.2 trillion, representing 34% of total debt.

- real estate, including land, was estimated to represent almost 70% of all tangible capital in 1963

- the taxable value of real property in the USA estimated at nearly US$16 trillion in 1991.

Byamugisha F (1999), referencing Jaffee and Renaud (1996) and Jefferies (1996)

Developing Countries

ECA Land Projects

From Adlington G, T Lamb, R McLaren, R Tonchovska (2021

- “Lead Author’s insight In one Central Asian country where we implemented a project, the local banks almost never lent money using property as collateral in the early years of the project. At the end of the project, I went back to the same banks, and they had a mortgage department in place dealing with customers every day. When asked about their lending portfolio, they said it was mainly small loans (but some large ones too) for short periods of a couple of years. I asked why their portfolio had grown so much and why they made the effort to register small loans like that. Their response was that the person coming for credit had to have a viable business plan, but the title document told them that the person was local and had roots in the community, which made them less of a risk. Also, it was so simple and cheap to register a mortgage that they just did it, because it gave them that extra bit of security. If people are borrowing in large numbers for business purposes, that gives some indication that the system is helping build the economy and that the customer is satisfied.”

From Torhonen, M (2016),

- From reported lessons learnt, some conditions that would likely result in titles being used as collateral are:-

- It is not axiomatic that economic benefits will result from LA projects. Complementary measures are likely needed (such as engagement with banks re their accepting titles as collateral).

- Institutional capacity to register changing rights and capture the resultant revenues needs to develop as further transactions accelerate in line with economic growth. Once the registers are complete, they should never need to be redone but must be maintained and updated

- A factor that contributed to success in many of the ECA projects was the emphasis on enhancing human resource capacity

- Flexibility in real time adaption is required during implementation

- Land issues are multidimensional, complex and diverse, successful interventions respond to a number of factors that are context specific

- Torhonen, M (2016) also noted:-

- Building an effective and sustainable LA system is a long term process, requiring long term commitment by the IC government and its development partners. Several tranches of assistance over a 15-20 year period have been used (by World Bank). If governments are not willing to commit to long term programs and to allocate the necessary budget, then the benefits from land titling projects may not be achieved or sustained

- Experience indicates that LA projects make more progress when a basic legal and policy framework exists before project interventions

From de Soto (2000)

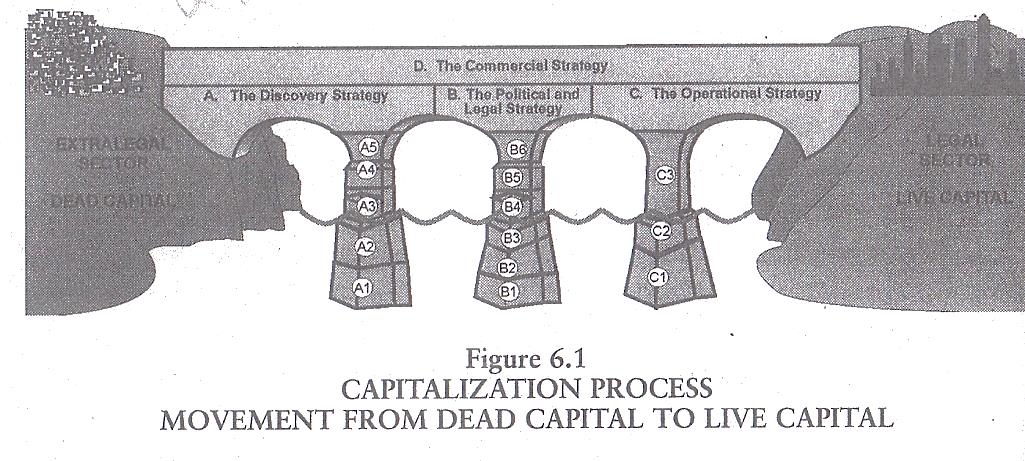

The central thesis of de Soto is that most of the poor already posses the assets they need to make a success of capitalism but their rights to possession are not adequately documented to use as collateral for a loan. de Soto depicted what he called the “capitalisation process” to convert dead capital to live capital in Figure 6.1 (shown below) in his book. The “bricks” in each pilar are listed in his book. de Soto’s thesis attracted criticism at its time.

An interesting exercise would be to use the SD approach to explore de Soto’s thesis and Figure 6.1 to identify insights. An analogy would be the testing of bridge design by simulation to determine if it would carry the desired loads.

ANNEX G

| Abbreviation | Meaning |

|---|---|

| CBA | Cost Benefit Analysis |

| ECA | Europe and Central Asia |

| IC | In-Country |

| KPI | Key Performance Indicator |

| LA | Land Administration |

| LO | Land Office |

| LR | Land Registry |

| NGO | Non-Government Organisation |

| PI | Performance Indicator |

| PIO | Performance Improvement Objective |

| POT | Performance over Time |

| PIP | Proposal to Improve Performance |

| PGov | Provincial Government |

| RGL | Registry of Government Land |

| SCS | Schematic of the Core Structure |

| SD | Strategy Dynamics |

Footnotes

- 1 As in previous chapters, the term “title” is used generically to indicate the documentation indicating registered property rights ↩

- 2 Quality of Titles is used in this chapter for simplicity and equivalent to Overall quality (assist economic development) from Chapter 11, and Annex A to this chapter ↩

- 3 The pilot aims to increase the Quality of Titles from ~0.3 to 0.95. This PIO is largely under the control or influence of the Provincial Government. ↩

- 4 This implies that the LR can cope with the increase in processing from having to register mortgages on a title ↩

- 5 S1- Banks lend very conservatively & LR maintains a very high Quality of Titles. S2- Banks lend less stringently; LR maintains a very high Quality of Titles; S3- S2 + an increase in titleholders; LR maintains a very high Quality of Titles ↩

- 6 Chapter 9 showed how the retention of a small % of revenue collected can provide the necessary extra funding for sustainability. ↩